Home > Insurance Blog > The renters insurance rundown: what most renters are missing out on

Despite the growing tenant base in the United States, only a minority of renters maintain renters insurance. This indicates an opportunity for property insurers to access an untapped customer base. In order to captivate a tenant’s attention, insurers must understand why tenants do not carry this insurance and then communicate the benefits of this coverage. Most notably, tenants need to understand the importance of coverage for personal contents, temporary housing, and liability. In this article, we review the components of landlord insurance compared to renters insurance as well as recent trends in hopes that insurers can better understand how to convince tenants of their need for insurance to protect their property and assets.

Landlord insurance

Many tenants believe that since they do not own the property, insurance is not necessary for them. However, this is not the case. Below is a list of items covered and not covered for a rental unit under a landlord’s property insurance policy.

- Dwelling – the dwelling coverage responds to pay for the Landlord’s expenses required to repair a rented home, condo, or apartment after it is damaged by a covered loss such as fire, lightning, wind, or hail.

- Liability – this coverage responds to pay medical or legal expenses if someone else sustains an injury at the rental property and the Landlord is responsible. An example is if a tenant falls down the stairs after a Landlord failed to repair a faulty rail, then the Landlord may be liable for the tenant’s medical expenses.

- Other structures – a Landlord’s rental unit may have detached structures such as a garage, workshop, or fence. This coverage pays for expenses required to repair these structures following damage from a covered loss.

- Landlord’s personal property used to service the rental – a landlord may have personal property at the rental unit such as yard equipment or home maintenance equipment. This coverage pays expenses if this equipment sustains damage from a covered event. This does not, however, cover the landlord’s personal belongings, such as recreational or entertainment equipment.

Not covered under a landlord policy

- Tenants’ belongings – most of the personal possessions in a rental unit belong to the tenant and not the landlord. It is important to note then that a landlord’s insurance policy does not cover a tenant’s personal possessions if a covered event damages the possessions. Depending on the type of rental unit, the value of a tenant’s personal possessions may be significant. Therefore, in order to protect these personal possessions, tenants need a renter’s insurance policy.

- Equipment breakdowns – If a critical appliance breaks, then the landlord’s policy will not cover expenses related to repairing or replacing broken appliances.

- Shared property – Some landlords live in a property and then rent out a room or another floor to a tenant. If this is the case, then the landlord is likely not eligible for a typical landlord insurance policy. A landlord policy specifically covers “non-owner-occupied” property. Homeowners renting out a portion of their property should consider adding a rider to their homeowners insurance policy in order to cover this exposure.

Renters insurance

Renters insurance remains a low-cost product that adds significant protection for tenants. In fact, the average renter’s insurance premium is only $180 per year or $15 per month. A renter’s insurance policy helps bridge the gap to make sure tenants have adequate property and liability coverage for those items not covered under a landlord’s policy. Below is a list of four items covered under most renter’s insurance policies.

- Personal property damage – this portion covers a tenant’s personal property if damaged in a covered event, such as fire, wind, or theft.

- Personal liability – this covers the tenant if someone else sustains an injury on the premises and blames the tenant for the event. The policy covers liability costs, including the costs of your legal defense.

- Medical payments – the renter’s policy provides some coverage for medical costs if someone is injured on tenant’s premises.

- Additional living expenses – If a covered event damages the rental unit such that the tenant can no longer occupy it, this coverage responds to pay living expenses beyond normal living expenses.

The additional living expenses coverage represents one of the most important components of renter’s insurance policy. As mentioned above, this coverage helps tenants pay for temporary housing in the event that their rental unit is not habitable following a covered peril. In the event of a property loss, the Landlord is responsible for repairing the damage to ensure the rental unit is safe and habitable. The Landlord is not required to provide temporary housing for the tenant. This is why the additional living expenses coverage is so important. An uninsured tenant will need to arrange and pay for their own temporary housing, while an insured tenant will work with their insurer’s temporary housing company to quickly arrange temporary housing following a loss. Temporary housing companies such as Sedgwick’s temporary housing division, provide quality temporary housing services for people displaced from their home.

Trends influencing the rental insurance market

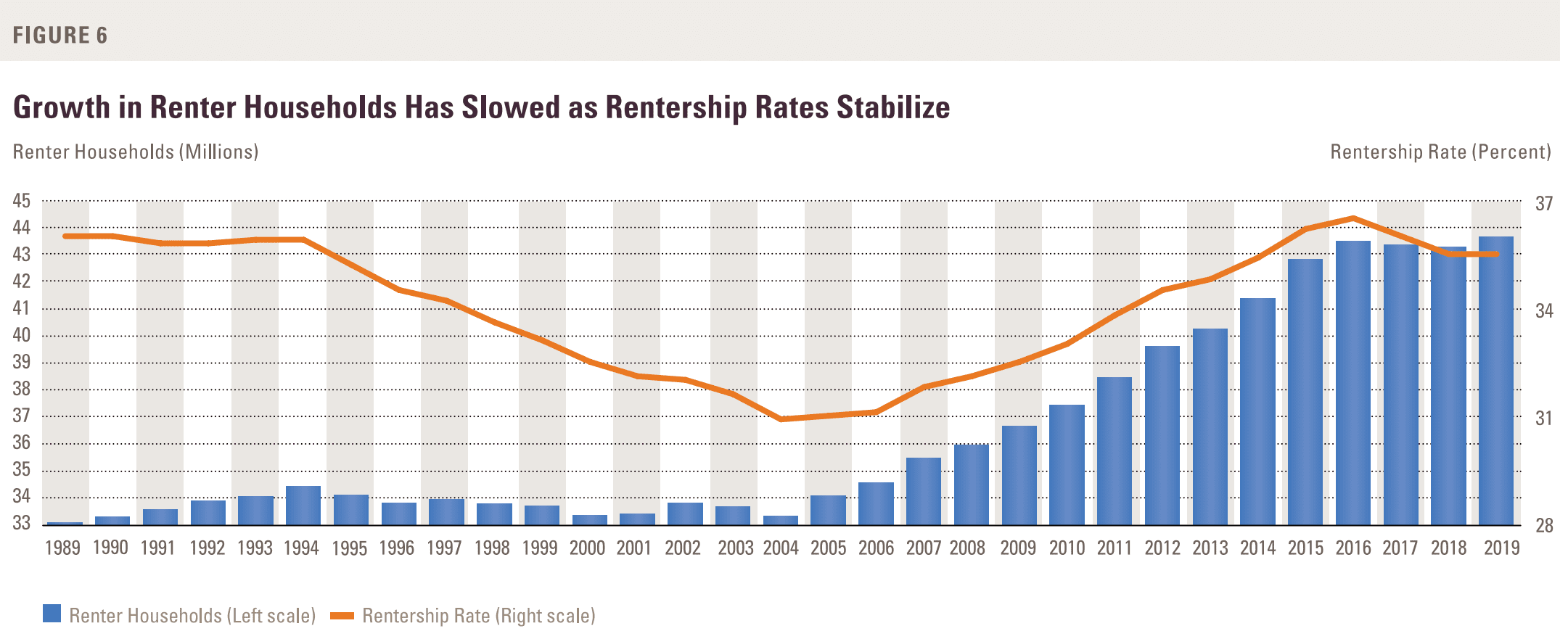

Despite the growing number of renters in the US, only 37% of renters have insurance. Several trends influence the renter’s insurance market; therefore, it is important for insurers to understand these factors.

The Joint Center for Housing Studies of Harvard University recently published a report “America’s Rental Housing 2020” source (January 2020), which identified some trends that directly impact the renters insurance market. Below are two examples.

Increase in the number of renter households – the total number of renters in the US increased significantly over the past 15 years. This created a large number of tenants, the majority of which do not have renters insurance. This trend created a significant opportunity for insurers.

Source: JCHS tabulations of US Census Bureau, Housing Vacancy Surveys.

Increase in the number of renters among high-income households – the below chart illustrates the recent growth in the number of high-income renters. While the total number of renters has stabilized in recent years, the number of high-income renters increased significantly. Insurers must pay attention to this trend. High-income earners can afford the additional cost of renters insurance more than lower-income renters can. Furthermore, high-income earners typically have more personal property that needs insurance.

These trends should energize insurers to take notice of the opportunity to serve new customers and help uninsured tenants understand how renters insurance can help secure their financial future.